- 529 basics for Iowa savers

- Why consider an out-of-state plan?

-

How we picked the six stand-outs

- 1. Illinois Bright Start 529: best mix of low fees and strong oversight

- 2. Utah My529: lowest fees and build-it-your-way flexibility

- 3. Ohio CollegeAdvantage 529: widest investment menu at a bargain price

- 4. New York 529 Direct: simplest, cheapest set-it-and-forget-it option

- 5. Nevada Vanguard 529: pure index investing for Vanguard loyalists

- 6. Virginia Invest529: standout safety options plus modern usability

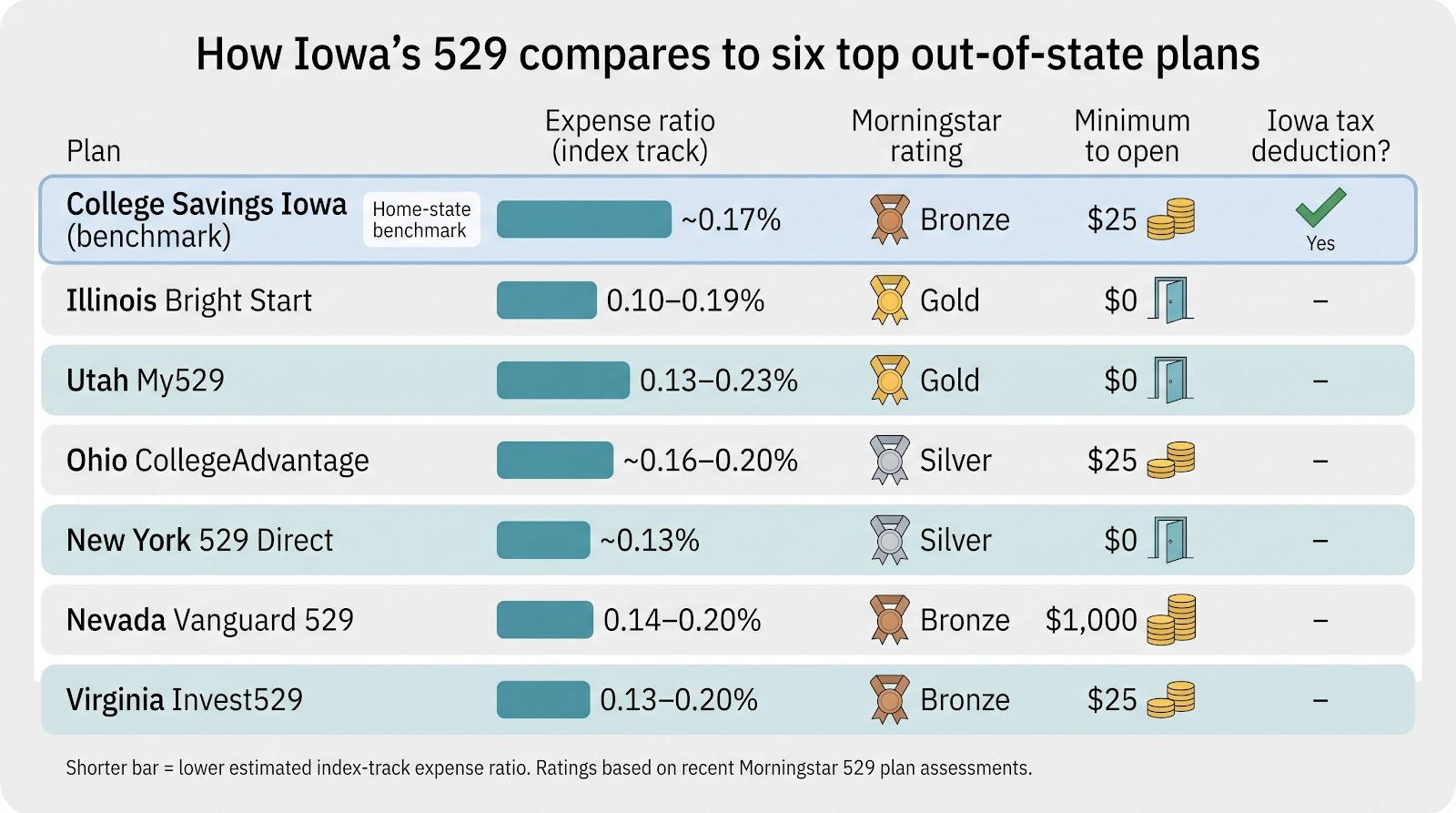

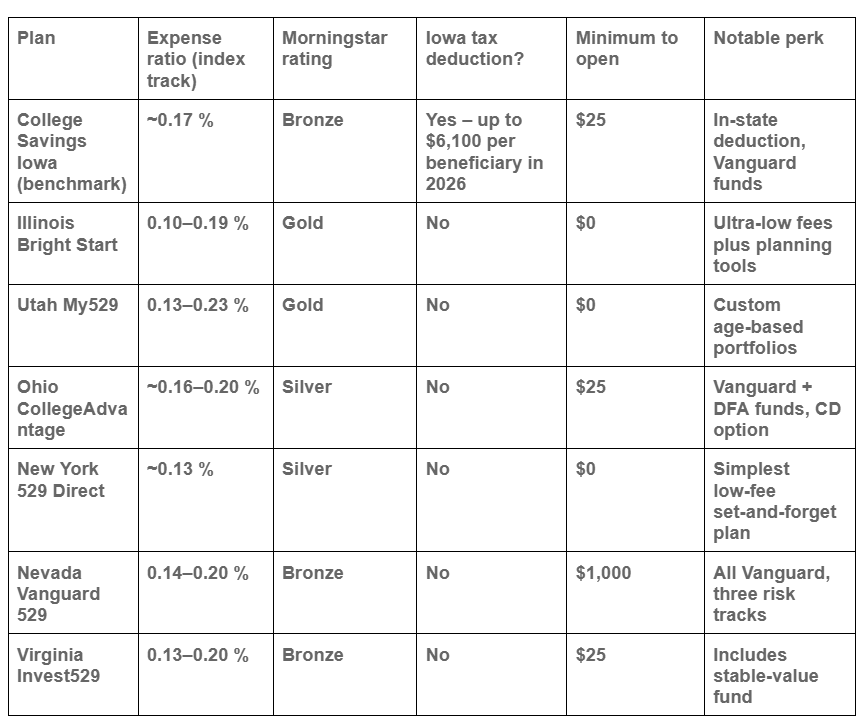

- How the six plans stack up at a glance

- FAQs Iowa parents ask every spring

- Conclusion

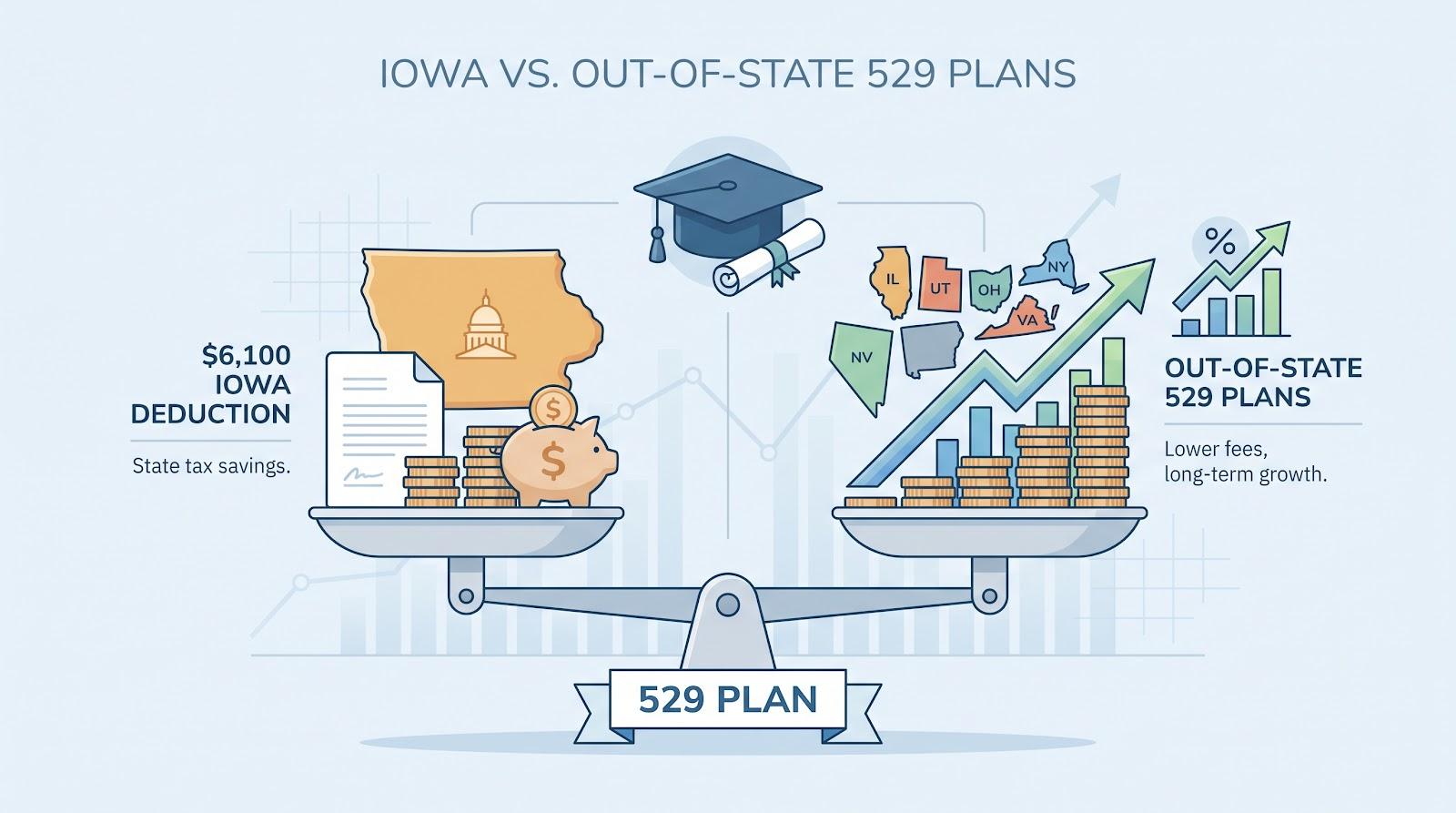

Iowa’s 529 tax break is generous—up to $6,100 per beneficiary in 2026 and indexed higher each year. Yet many families still ask whether a lower-fee, stronger-performing plan in another state can leave them with more college money.

In this guide, we unpack that trade-off and rank the six out-of-state 529 plans that give Iowa savers the best long-term value. To see the math for yourself, plug a few scenarios into this college planning calculator; it shows exactly how lower fees—or losing the deduction—shift your final balance.

First, a quick primer on 529 basics for Iowa investors, then the plan-by-plan breakdown.

529 basics for Iowa savers

A 529 plan is a state-sponsored investment account that lets your money grow tax-free when you use it for qualified education costs such as tuition, fees, books, and room and board.

At the federal level, every plan follows the same rules: there is no upfront deduction, but earnings and qualified withdrawals remain tax-free.

States layer on their own incentives. Iowa offers a $6,100 per-beneficiary contribution deduction for 2026, and that cap rises each year. To claim it, contributions must go into College Savings Iowa or the advisor-sold IAdvisor plan. Put the money in Utah’s My529 and the deduction disappears.

Plan geography never limits where your child studies. You could fund a New York 529 today and pay tuition at the University of Iowa tomorrow, or use an Iowa account for a semester in Tokyo as long as the school has a federal code.

The takeaway: the federal tax break is identical nationwide, but only an Iowa plan unlocks your state deduction. Everything else, including fees, fund menus, and ease of use, varies by state.

Why consider an out-of-state plan?

Iowa’s tax break looks generous. Drop $6,100 per child into College Savings Iowa and you shave 3.8 percent off your state bill, roughly $232 in instant savings.

So why do thousands of Hawkeye families still park extra college dollars in Utah, Illinois, or New York?

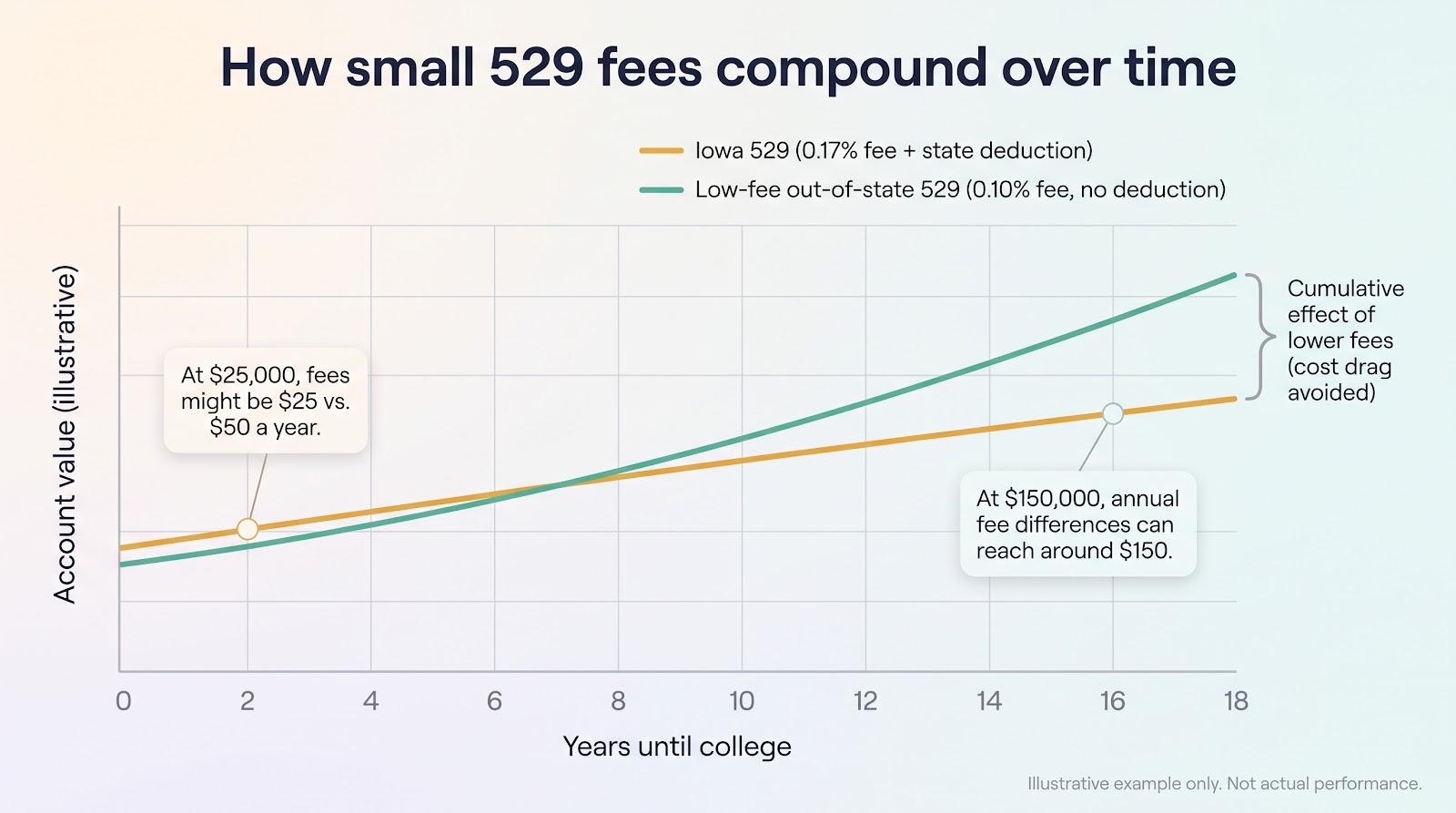

The reason is cost drag. Every 529 charges an expense ratio that quietly skims a slice of your balance each year. Iowa’s direct plan sits near 0.17 percent, while the nation’s leanest options (Bright Start or My529) hover around 0.10–0.13 percent.

At $25,000, that tenth-of-a-percent gap feels small: $25 versus $50 a year. Let the account grow to $150,000, realistic for twins in middle school, and the annual fee difference climbs to $150. Stretch that over a decade of compounding and the lower-cost plan can reclaim far more than the deduction you gave up.

Performance matters too. Plans that blend low fees with strong oversight often earn Morningstar Gold or Silver medals, while Iowa’s plan currently holds Bronze. Over long stretches, that quality edge may add a few tenths of a percent to annual returns, boosting growth the same way fee savings do.

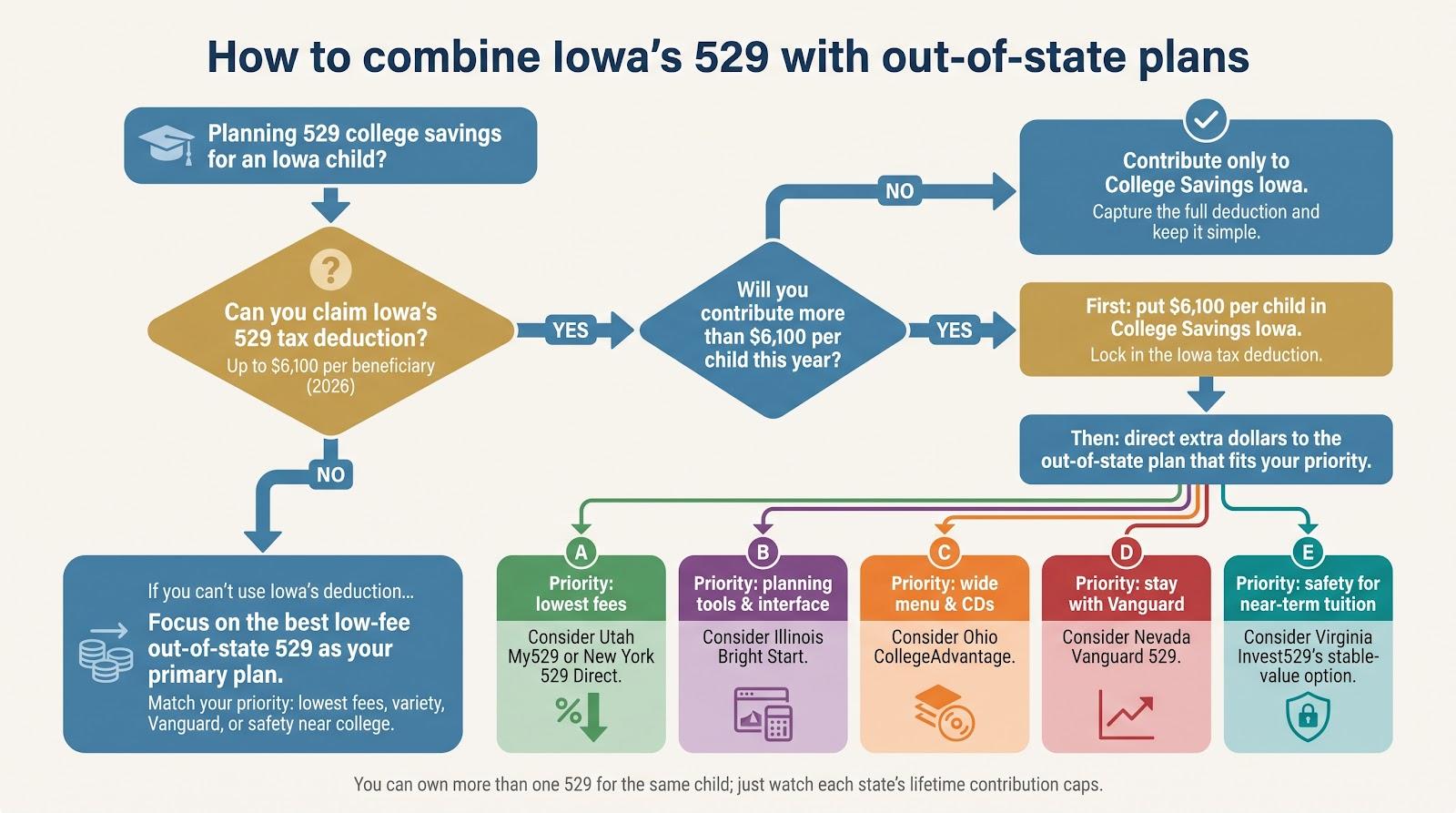

If you contribute only enough to claim the deduction, Iowa remains the easy choice. Once you invest beyond that threshold, or if you want the absolute lowest costs and broader fund menus, a top out-of-state plan can still leave you with more college money despite losing the tax perk.

Many families split the difference: send the first $6,100 per child to Iowa each year, then direct any extra dollars to a low-fee out-of-state plan. You keep today’s tax win and still capture long-run efficiency, a strategy we see often among fee-savvy Iowa parents.

How we picked the six stand-outs

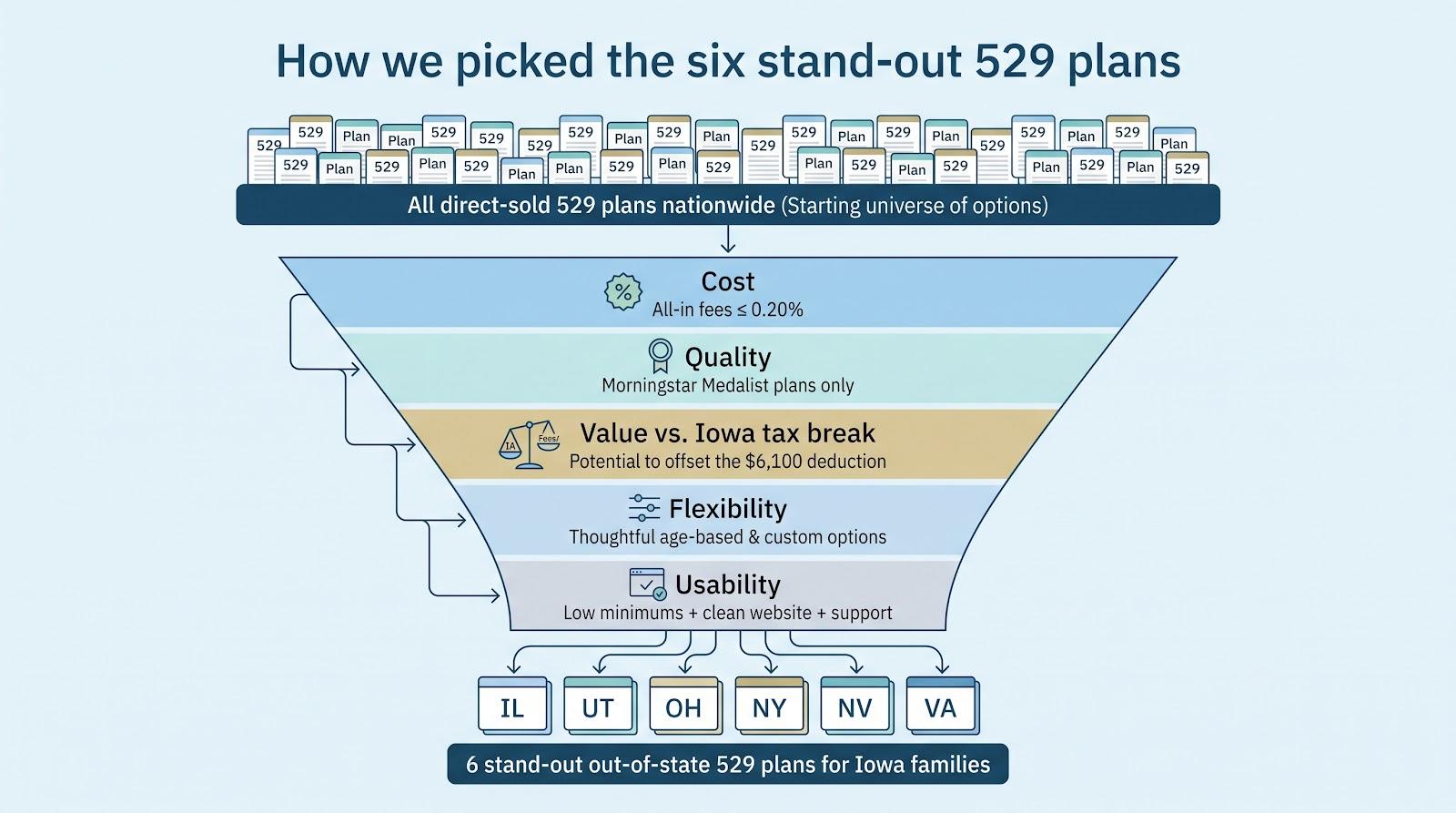

A big claim, “best,” needs a clear yardstick. We started with every direct-sold 529 plan available nationwide and scored each one on five factors that matter to Iowa families.

First came cost. Lower expense ratios lift your child’s balance, so we cut any plan with an all-in charge above 0.20 percent.

Next was quality. We relied on Morningstar’s annual 529 medals, which rate stewardship and long-term performance. Only Medalist plans (Gold, Silver, or Bronze) made the cut.

Third was value versus Iowa’s tax break. If lower fees or better returns could not reasonably offset giving up the $6,100 deduction, we dropped the plan.

We then weighed flexibility. Plans earned extra credit for menus that let you fine-tune risk, such as multiple age-based tracks or a custom glide path, without adding complexity.

Finally, we judged usability: low minimums, a clean website, and responsive customer service.

After tallying the scorecards, six plans stood out. The next section breaks them down one by one and shows where each shines.

1. Illinois Bright Start 529: best mix of low fees and strong oversight

Bright Start earns the top spot because it balances low pricing with a proven investment team.

The index portfolios cost 0.10–0.19 percent, roughly half the drag in Iowa’s direct plan, and College Planning Calculator illustrates how shaving even a few basis points can snowball into thousands more for tuition by freshman year.

Morningstar analysts back up the math, awarding Bright Start a Gold medal in their latest 529 sweep, a level shared by only a handful of state plans nationwide.

Opening an account is easy. A $0 deposit gets you started, and the online dashboard feels straightforward. Three age-based risk tracks let you pick an aggressive, moderate, or conservative glide path. Prefer to tinker? Static options and single-fund portfolios give you granular control.

The trade-off for Iowans is the lost state deduction because dollars land outside College Savings Iowa. Many families solve that by maxing the $6,100 deduction at home, then sending extra savings to Bright Start for its lower annual costs.

If you value simple interfaces, Vanguard-level fees, and independent validation from Morningstar, Bright Start belongs on your shortlist.

2. Utah My529: lowest fees and build-it-your-way flexibility

If your goal is to squeeze every penny of cost out of college investing, Utah’s My529 is tough to beat. Its index portfolios start at 0.13 percent, about half Iowa’s all-in charge and among the cheapest nationwide.

Cost is only half the appeal. Utah lets you design a custom age-based glide path, adjusting exactly when and how the mix shifts from stocks to bonds. Seasoned DIY investors enjoy that control, while hands-off savers can choose one of four preset enrollment tracks that gradually dial down risk.

Morningstar analysts rewarded this mix of low pricing and smart oversight with a Gold medal, the firm’s highest conviction rating. In plain language, they expect My529 to outperform most peers over a full market cycle.

Opening an account is simple. There is no minimum deposit, and the site guides you through a brief risk quiz before funding. Add reliable customer service from the Utah Board of Higher Education, and you have a strong “second bucket” once you have maxed the Iowa deduction.

Some savers want more than plain index funds. Ohio’s CollegeAdvantage delivers that variety without drifting into high costs.

Its core age-based tracks run roughly 0.16 to 0.20 percent, still in low-fee territory. Behind those numbers sits a lineup that pairs Vanguard index funds with Dimensional Fund Advisors smart-beta options and even FDIC-insured bank CDs. You can keep one child in a market-tracking glide path while parking another’s senior-year tuition in a guaranteed CD, all within the same account.

Morningstar analysts call that mix “thoughtful and investor-friendly” and awarded the plan a Silver medal in their latest survey. Fees stay moderate even when you select DFA portfolios, a rarity among plans that offer factor tilts.

Opening an account costs $25. The website feels dated next to Utah’s portal, but navigation is straightforward and customer service responds quickly. Ohio also runs occasional promotions, such as a $25 or $50 bonus for starting automatic contributions, which make a low opening balance easier.

If you want freedom to fine-tune risk without paying active-fund premiums, CollegeAdvantage is a versatile choice among 529 plans.

4. New York 529 Direct: simplest, cheapest set-it-and-forget-it option

If you want a low-maintenance plan, New York’s direct program stands out.

Its age-based portfolios hover around 0.13 percent, matching Utah for the lowest price tag in the country. Every underlying fund is a Vanguard index fund, so you are buying the market with no added extras.

That focus on cost and simplicity earned the plan a Silver medal from Morningstar analysts, who cite its “exemplary stewardship and price advantage” as key strengths.

Opening an account requires no minimum deposit. The single enrollment-date track then shifts from stocks toward bonds as college nears. You will not find multiple risk flavors or active strategies here, and that is the point. The website is plain, but automatic contributions and gifting links work smoothly.

For Iowa savers who prize low friction and minimal fees, New York 529 Direct offers a clean, no-decisions path to long-term growth.

5. Nevada Vanguard 529: pure index investing for Vanguard loyalists

Some investors like every account under one roof. Nevada’s Vanguard 529 lets you do that while staying in the low-fee camp.

All portfolios use classic Vanguard index funds, and total expenses run 0.14 to 0.20 percent, a bit above New York’s plan but still well below Iowa’s. Morningstar’s team rates the program Bronze, praising its “straightforward, low-cost approach.”

Flexibility comes from three age-based tracks (aggressive, moderate, conservative) plus roughly twenty static options. You can remain hands-off with an enrollment-date fund or build a custom mix without leaving Vanguard’s familiar lineup.

The catch is the entry ticket. Opening an account takes a $1,000 lump sum, lower than Vanguard’s usual mutual-fund minimum. If you plan to contribute small amounts each month, start elsewhere and roll over once you clear the threshold.

For families already using Vanguard for IRAs or brokerage accounts, the convenience of seeing your 529 on the same dashboard—and knowing every dollar sits in index funds—can outweigh the higher minimum and slightly higher fee.

6. Virginia Invest529: standout safety options plus modern usability

Virginia’s direct plan rounds out our list by pairing low-cost index tracks with something rare in 529 plans: a true stable-value fund that targets bank-like returns while protecting principal.

Index portfolios cost roughly 0.13 to 0.20 percent, keeping them on par with Ohio and Nevada. Recent fee trims and solid governance helped the plan earn a Bronze medal from Morningstar’s analyst review.

Why does the stable-value sleeve matter? When college is two or three years away, even a mild market dip can disrupt tuition plans. Parking part of the balance in Virginia’s capital-preservation option locks in a yield that has hovered around three percent, higher than most money-market choices, without exposing the funds to bond-price swings.

The platform feels user-friendly. A $25 deposit opens the door, the interface works well on mobile, and live chat connects you to a real person. Active-fund choices are available but pricey; stick to the index or stable-value menus to keep costs tight.

For Iowa families approaching freshman year, that blend of low-fee growth tracks and a shelter for near-term dollars makes Invest529 a practical final addition.

How the six plans stack up at a glance

Numbers matter more than adjectives. The table below lists the key stats Iowa savers ask about most—fees, ratings, and minimums—and sets each out-of-state pick against College Savings Iowa for context.

Use the table as a quick check. If a plan’s lower fee and features do not offset the roughly $232 state tax benefit on each $6,100 Iowa contribution, keep that slice in the home-state plan and direct extra dollars to the low-cost option that best fits your style.

FAQs Iowa parents ask every spring

Can I claim the Iowa tax deduction with any of these six plans?

No. Iowa allows a deduction of up to $6,100 per beneficiary each year only when the contribution lands in College Savings Iowa or its advisor-sold twin. Out-of-state deposits receive no state relief, so weigh that $232 tax benefit against possible fee savings elsewhere.

Will my child have to attend college in the plan’s state?

No. A 529 from Utah, New York, or any other state pays qualified bills at any accredited U.S. (and many foreign) institution. The plan’s zip code affects taxes and oversight, not where the funds can be used.

Can I own more than one 529 for the same child?

Yes. Many Iowa families grab the deduction on the first $6,100 in the Iowa plan, then send extra dollars to a lower-cost option such as Bright Start or My529. There is no federal penalty for holding multiple accounts; just stay under each state’s lifetime contribution cap.

What happens if my child earns a full scholarship?

You have three choices: move the money to another family member, withdraw up to the scholarship amount penalty-free (taxes on earnings still apply), or, starting in 2024, roll up to $35,000 into the beneficiary’s Roth IRA, subject to annual limits under SECURE 2.0.

If I roll my Iowa 529 into another plan later, do I keep past deductions?

No. Iowa will reclaim the deductions you previously claimed by adding that amount to your taxable income in the year of the rollover. For most savers, it is smarter to leave existing dollars in place and direct new money to the outside plan instead.

Conclusion

Start where the numbers make sense. Use Iowa’s plan for the deduction if you can. Then, if lower fees or special features tip the scale, open a second account in the out-of-state plan that best fits your goals.